European stock markets inched lower in early trade Monday after a broadly lower session for Asian equities. Heading into the last three trading days of the quarter, the FTSE 100 is up ~1.5% in June and almost +6% for the quarter as it holds above 7,100. Sentiment may be cool this morning but it’s been a solid turnaround from last Monday, when it struck 6,950. US futures are little changed after the S&P 500 notched a fresh record on Friday and enjoyed its best week since February. Core PCE inflation was a tad cooler than expected, giving investors the green light to give equities some bid despite the myriad risks on the horizon, including rising Covid cases in Asia. There is also a strong hope that President Biden’s $1tn bipartisan infrastructure deal will be passed. Over the weekend the president himself rowed back on his earlier suggestion that a deal would be dependent on also passing the Democrats’ tax plans, and that he could veto the infrastructure agreement. The next big risk event is Friday’s jobs report for the US, which is expected to show employers added 700,000 jobs in June. The nonfarm payrolls report is central to the market’s expectations for Federal Reserve policy, since the labour market is still the most important consideration for officials as they seek to time the start of the tightening process. The US economy is still roughly 7m jobs short of where it was before the pandemic. It makes a big difference to the timing of tapering/tightening whether we see 700k or 350k each month. The last couple of prints have disappointed.

On the companies front, Burberry shares slumped 9% after CEO Marco Gobbetti said he’s moving on. It presents near-term risks – investors will want to know who takes over the reins and whether there is change in strategy. Given the consolidation in the luxury sector, and the current valuation vs peers, it could be a target. Whilst there are some pandemic-related issues still being washed out, Burberry remains a strong brand in the luxury space with room to appeal to a broader consumer base over the coming years.

At the other end of the food chain, Greggs is confident that performance will be strong even as the pent-up demand for retail subsides and hospitality businesses like cafes and restaurants can compete more effectively. Since May 10th, like-for-like sales growth at company-managed stores was at between one and three per cent when measured against the same period in 2019. The company said that ‘this level of sustained sales recovery is stronger than we had anticipated and, if it were to continue, would have a materially positive impact on the expected financial result for the year’. Shares opened about 2% higher and are up 47% YTD.

Oil advanced to its highest in almost three years ahead of this week’s OPEC+ meeting. The market remains tight amid OPEC’s self-restraint and the inability of US drillers to ramp up output. Whilst the rig count rose to 470, according to the latest Baker Hughes data, that’s well below the ~800 at the beginning of 2020. As for OPEC+, the chatter is focused on the cartel increasing production by half a million barrels per day. Less than that would be a green light for prices to rally. OPEC has been sounding optimistic about the demand outlook but the emergence of high numbers Covid cases in Asia should mean it remains relatively restrained at this meeting. Meanwhile it is looking unlikely the US will lift sanctions on Iran any time soon after the country missed a deadline to renew its atomic monitoring pact with international inspectors, which follows the election as president of the hard-line cleric Ebrahim Raisi. The US has launched airstrikes on two Iran-backed militia groups on the Syria-Iraq border area.

Crypto markets are bullish this morning with broad gains. Bitcoin futures trade about +9% at $35k but the 200-day SMA is key resistance. It comes as the FCA bans Binance, the largest crypto exchange in the world, from operating in the UK. More clampdowns coming.

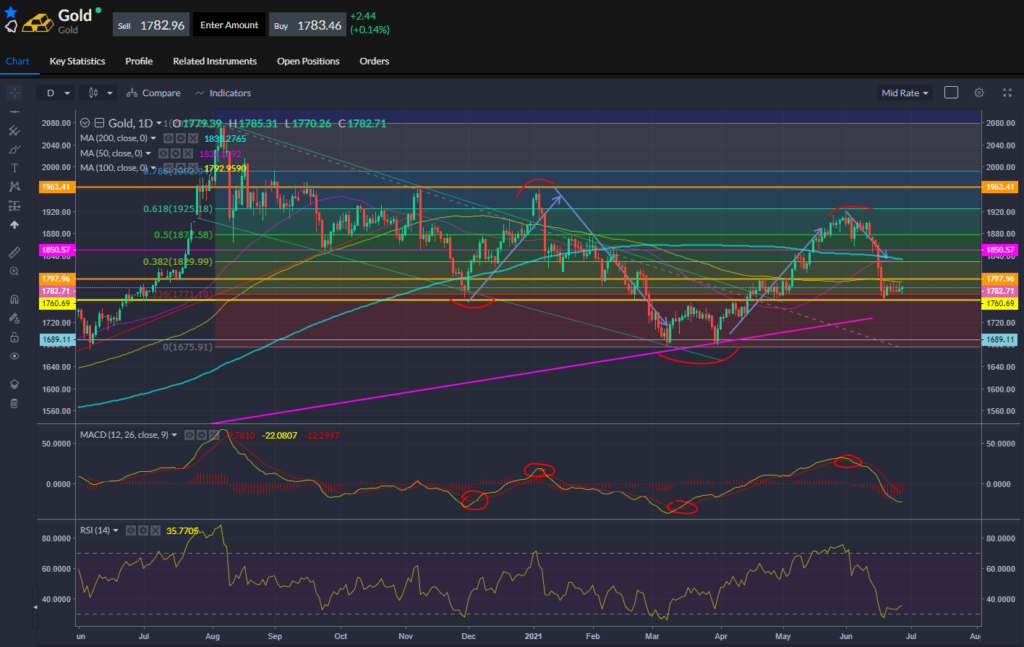

Gold: Going nowhere within the Jun 18th range for now – looking for the next move in rates to refocus.

GBPUSD: Starts the session higher but a break of the 200-hour SMA hit resistance.

Risk Warning: this article represents only the author’s views and is for reference only. It does not constitute investment advice or financial guidance, nor does it represent the stance of the Markets.com platform.When considering shares, indices, forex (foreign exchange) and commodities for trading and price predictions, remember that trading CFDs involves a significant degree of risk and could result in capital loss.Past performance is not indicative of any future results. This information is provided for informative purposes only and should not be construed to be investment advice. Trading cryptocurrency CFDs and spread bets is restricted for all UK retail clients.